Real IBC Story: Access $500k for Real Estate With Life Insurance

What Is a Multi-Generational Trust?

Who Needs Disability Income Insurance?

Infinite Banking Savings System

Family Banking Master Class

How To Prepare for Risks and Uncertainties with Life Insurance

5 Smart Ways to Spend Your Tax Refund

Retirement Savings

Best Disability Insurance for Physicians

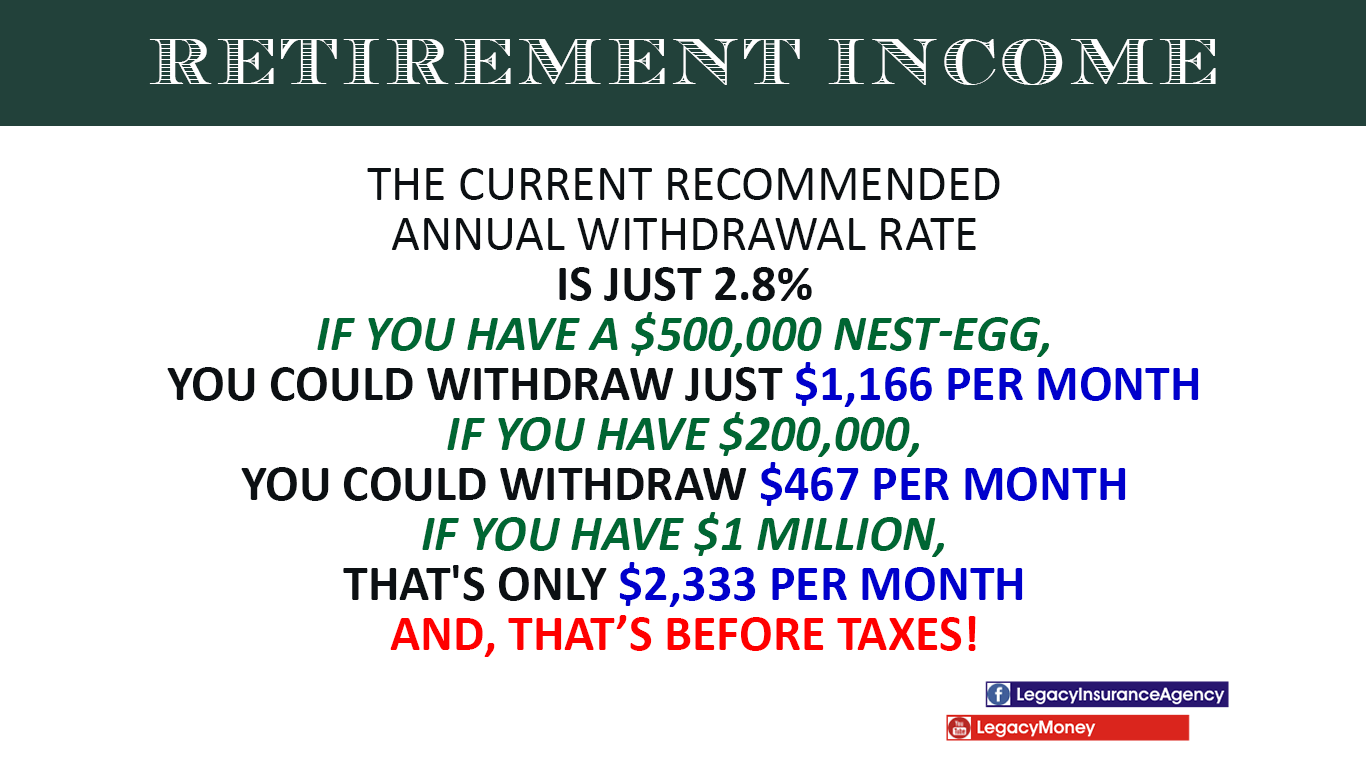

Retirement Income Distribution – How To Retire with More Spendable Income

Cash Value, Whole Life Insurance for Today

Retirement Planning with Life Insurance

Legacy Money Live

Risks of Disability

Financial Blog

Welcome to our financial blog. Stay up to date on financial issues. Readers will enjoy financial posts on a variety of topics from saving to tax diversification.

You can increase your knowledge and improve your Financial Intelligence by reading our blog. Read the latest financial news, and learn financial strategies for achieving financial success.

Personal Finance

Personal finance is the process of planning and managing income, expenses, saving, investing, risk and protection. Smart financial management will include a financial plan.

Scroll down for our latest blog and archives.

Our Mission

Our mission is to enrich the lives of families by providing a process for them to maximize their financial security by avoiding the eroding factors of money, and to promote financial intelligence by educating others with specialized knowledge.

Financial Education

Improve your financial education and increase your financial intelligence by expanding your knowledge, and you will increase your opportunities for success. Reading books and learning from others’ experience is the easiest way to build your knowledge base, shop our bookstore.

VLOG – Legacy Money Financial Video Blog

Legacy Money is our video blog and YouTube channel. The Legacy Money VBLOG is devoted to helping families and business owners protect themselves, plan for the future, and create generational wealth.

Learn more, subscribe to our YouTube channel: www.youtube.com/legacymoney

Let’s Talk

Get to know us, and discover what you may be missing with your no cost introductory call.